Introduction

When comparing contractor payments platforms, companies typically focus on the headline service fee. The reasoning is straightforward: the figure is in the price list, it is easy to compare across providers, and it fits cleanly into the budget.

In practice, that figure captures only part of the cost. The second, often larger, item is the hidden mark-up embedded in the currency conversion rate. It does not appear as a separate line on the invoice, in the tariff schedule, or in the contract. A company only becomes aware of it when it compares the rate the provider actually used for conversion with the mid-market rate on the same date.

This guide explains how the mark-up works, why it persists so reliably in cross-border B2B payments to distributed teams, and what the paying company itself can verify and act on.

How the hidden mark-up in the conversion rate works

Any cross-border payment in which the client's account currency differs from the contractor's account currency involves a conversion. At that moment, two rates come into play.

Mid-market rate — the rate at which banks and large financial institutions exchange currency between themselves. Closely related values are published by central banks (the ECB, Bank of England and others) and aggregated by XE.com, OANDA and Bloomberg.

Provider's rate — the rate the contractor payments platform actually applies when converting the client's funds into the contractor's payout currency.

The difference between these two rates is called the FX spread, or currency conversion mark-up. That difference, expressed as a percentage of the conversion amount, is the real FX mark-up.

Example. On a given date, the EUR/USD mid-market rate is 1.1883. When converting €10,000 into dollars, the contractor payments platform applies a rate of 1.1647. The converted amount comes to $11,647 instead of $11,883 at the mid-market rate. The $236 difference is 2% of the conversion amount. That $236 is not recorded anywhere as a "fee" or "additional charge"; formally, the client has only paid the service fee stated in the price list.

Across several dozen monthly payments in different currency pairs, the cumulative effect becomes material. A monthly contractor payments volume of €100,000 at a 2.5% mark-up in the rate means €2,500 per month, or €30,000 per year, in additional costs — with no separate line in the accounts.

What the numbers say: comparing two pricing models

A meaningful comparison between providers cannot stop at the headline service fee. A full comparison combines two components: the declared fee and the FX mark-up.

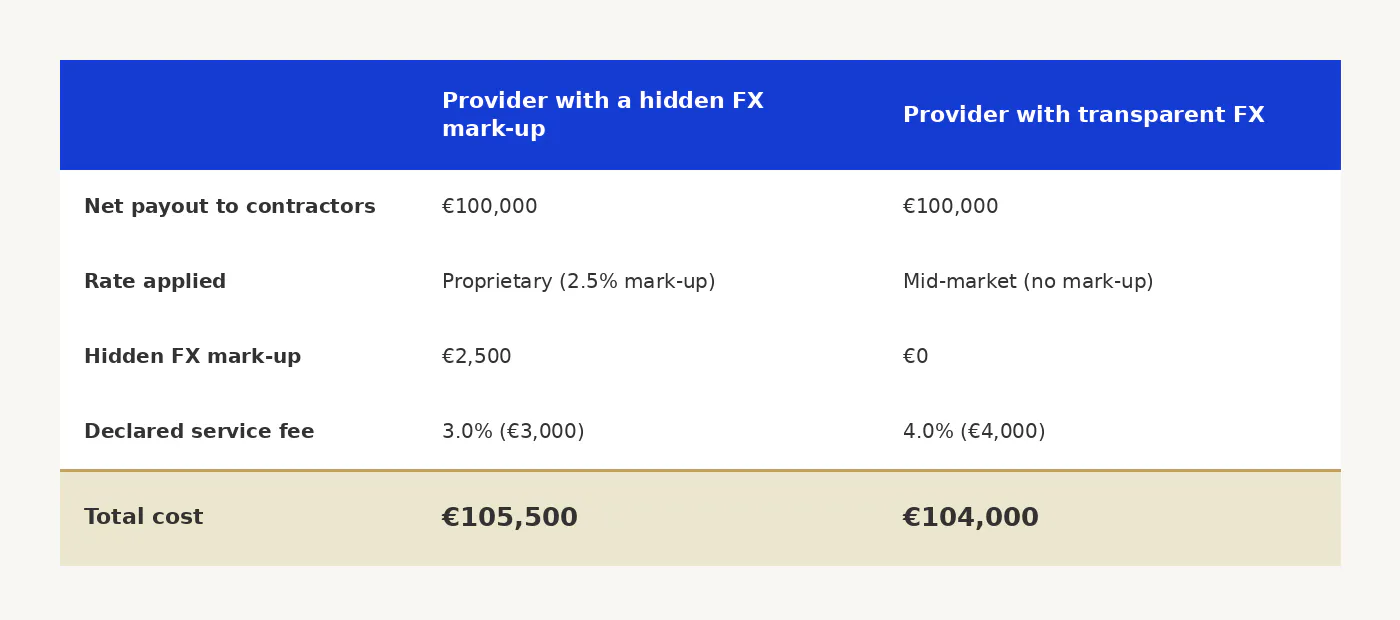

Suppose a company pays its contractors €100,000 in monthly equivalent, and the two providers under consideration differ both in their service fee and in their approach to FX.

On paper, the first provider looks cheaper: a 3% headline fee against 4% for the second. In practice, the total cost is €1,500 per month — or €18,000 per year — higher with the first, because part of the actual cost has been moved outside the declared tariff and built into the rate.

This gap between declared and actual cost is the key mechanic that sustains the commercial appeal of the hidden-spread model: the headline figure stays low, and the margin is recovered through the rate.

Cost of getting it wrong: with an annual contractor payments budget of €1.2 million (€100,000 a month), the difference between the two pricing models in this scenario is roughly €18,000 per year. Over three to five years, the accumulated cost is significant enough to affect the financials — without ever appearing as a separate line in management accounts.

Why transparency regulation does not close the B2B perimeter

A common question from finance leaders is: "If disclosure rules for FX mark-ups already exist in the EU, US and UK, why have hidden spreads not been driven out of the cross-border B2B payments market?"

The answer lies in the architecture of the regulatory regimes themselves: they are largely designed to protect the consumer, not the corporate payer.

European Union: PSD2, CBPR2 and the corporate opt-out

In the EU, the main FX-transparency requirements sit in two instruments: the Payment Services Directive (PSD2, Directive (EU) 2015/2366) and the Cross-Border Payments Regulation (CBPR2, Regulation (EU) 2019/518).

Article 45(1) of PSD2 requires payment providers, before initiating a single transaction, to disclose to the payer all fees, the applicable conversion rate, and the final amount that will be credited to the payee. CBPR2 adds a requirement to express the mark-up as a percentage over the ECB reference rate and to publish that figure on a publicly available electronic platform. The scope of CBPR2, however, is largely limited to card-based transactions (POS and ATM) and SEPA transfers within the EU/EEA — which, in itself, places a significant share of cross-border B2B contractor payments outside its reach.

Both instruments contain a critical limitation for the B2B sector. Under Articles 38(1) and 61(1) of PSD2, the parties may agree to disapply Title III (transparency and information requirements) and certain provisions of Title IV where the payer is not a consumer. In practice, this means that when the payer is a legal entity, the provider and the client may agree on bespoke disclosure terms, including terms less strict than those mandated for consumers.

Source: Recital 84, Directive (EU) 2015/2366

"In order to strengthen the trust of consumers in a harmonised payment market, it is essential for payment service users to know the real costs and charges of payment services in order to make their choice. Accordingly, the use of non-transparent pricing methods should be prohibited, since it is commonly accepted that those methods make it extremely difficult for users to establish the real price of the payment service."

The wording points squarely at the consumer angle: "trust of consumers", "their choice". The protection PSD2 affords to an individual sending money to family abroad applies in the B2B perimeter only where the parties have agreed it does — and very often, they have not.

United States: Regulation E and the B2B exclusion

In the US, the equivalent transparency requirements for cross-border transfers are set out in Regulation E, Subpart B (12 CFR Part 1005), known as the Remittance Transfer Rule. They require providers to disclose, in advance, the amount the recipient will receive, the rate applied and all fees.

The definition of "sender" in Regulation E, however, is unambiguous:

"a consumer in a State who primarily for personal, family, or household purposes requests a remittance transfer provider to send a remittance transfer to a designated recipient."

This definition explicitly excludes business-initiated transfers, including those by self-employed individuals. The protective framework the CFPB has built around consumer remittance transfers therefore does not apply to B2B contractor payments — even where the same providers that serve consumer remittance also work with corporate clients.

The rule also contains an absolute carve-out by amount: transfers of $15 or less are not covered at all.

United Kingdom: Payment Services Regulations 2017

In the UK, PSD2 was transposed into national law through the Payment Services Regulations 2017, which implement the FX-transparency requirements among others. Following Brexit, the core scope has been retained, and the FCA continues to examine initiatives to strengthen FX transparency in cross-border payments. Structural limitations comparable to those in the EU — the absence of a hard, mandatory protection in the B2B perimeter — remain in the current regime.

What is changing: PSD3 and PSR

The PSD3 and new Payment Services Regulation (PSR) package — on which the European Parliament and the Council of the EU reached political agreement in late November 2025 — explicitly recognises the FX mark-up as a charge subject to disclosure. The core FX-transparency requirements are being moved into the PSR, a directly applicable regulation, which removes the national divergences seen in transposition. The European Fintech Association (EFA) and several major market participants are additionally lobbying for an aggregated mid-market benchmark to be used in place of the ECB reference rate. On current estimates, formal publication in the EU Official Journal is expected in the first half of 2026, with application following 18 months after publication — roughly 2027–2028. Until then, B2B-provider market practice remains as it is.

The combined practical effect.

As of 2026, neither the EU, the US nor the UK has a regulatory regime that automatically shields the corporate payer from an opaque FX mark-up in contractor payments. Disclosing the real FX spread is a step the company itself has to initiate — at the point of choosing a provider, and in the contractual terms.

How to calculate the real FX mark-up yourself

A self-check does not require any financial software. One actual payment, access to the provider's statement, and an online source of mid-market rates are enough.

- Pick one contractor payment from the last 30 days. Note the date of conversion, the source currency, the payout currency and the amount.

- Identify the rate the contractor payments platform used for conversion. Most providers are required to show this information in their reporting or in the client portal. If it is not available, request it explicitly.

- Find the mid-market rate for the same date. Sources: the ECB (ecb.europa.eu) for EU pairs, XE.com, OANDA, Bloomberg. It is best to use a rate set in the middle of the trading day (the ECB fixing at 14:15 CET, or the London close at 16:00 London time).

- Calculate the mark-up. Formula: (mid-market rate − provider's rate) ÷ mid-market rate × 100%. The result is the FX mark-up percentage for that specific transaction.

- Scale to monthly and annual volume. Multiply the percentage by your monthly contractor payments volume — this gives the actual monthly FX mark-up. The annual figure is twelve times larger.

Reference points for interpreting the result:

- Below 0.3% — close to the market benchmark: real mid-market FX with no mark-up, or a minimal one.

- 0.3–1.0% — typical for reputable fintech providers and banks operating in the EUR/USD corridor.

- 1.0–2.5% — the mainstream practice among B2B contractor payments platforms.

- Above 2.5% — a high mark-up; on an annual basis, it generally exceeds the declared service fee.

If the result falls into the last two categories, it is worth reopening the question of the provider's real cost relative to alternatives.

What to look at when choosing a provider

FX transparency is a necessary but not a sufficient requirement when choosing a contractor payments platform. A real mid-market rate saves the company the FX mark-up by itself, but it does not address other critical perimeters. The full picture of the choice requires verification of the following:

- FX policy — a real mid-market rate with no hidden mark-up, or a clearly disclosed mark-up with a stated rationale.

- Correct legal structuring of contractor relationships — Contractor of Record (COR), Employer of Record (EOR), Merchant of Record (MOR) models with confirmed legal coverage in the jurisdictions where contractors operate.

- Documentation for every transaction — invoices, acceptance certificates and tax forms, all ready for audit and bank queries.

- The provider's legal structure and sanctions hygiene — no routing through sanctioned banks, a clean jurisdiction for the parent company, no adverse media.

- A payment model without pre-funding — no requirement to maintain "trapped" balances at the provider, which distort cash flow in the financials.

Each of these perimeters shapes the total cost of working with a provider — financial (fees and FX), regulatory (sanctions, tax, contractor reclassification), reputational (loss of banking relationships, investor due diligence) and operational (speed and reliability of payment). A decision based solely on the headline percentage fee inevitably misses most of this picture.

Conclusions

The hidden FX mark-up in contractor payments is not a marketing curiosity or a quirk of particular providers. It is a stable industry practice, sustained by a combination of economic, competitive and regulatory factors:

- FX-spread income is often no smaller than income from declared service fees;

- the headline percentage fee remains the primary point of comparison when choosing a provider, which works in favour of those who hide part of the cost in the rate;

- FX-transparency regimes (PSD2, CBPR2, Regulation E, the UK Payment Services Regulations 2017) primarily protect the individual consumer rather than the corporate payer, and in the B2B perimeter they apply with material carve-outs.

In the absence of automatic regulatory protection, responsibility for surfacing the real cost of payment sits with the company itself. The check takes a few minutes on a single transaction and requires no specialist tools. The annual impact is typically anywhere from thousands to tens of thousands of euros or dollars depending on volume — comparable to a meaningful share of a company's current financial costs.

Finboo is built on the opposite principle: a mid-market rate with no hidden mark-up, and a transparent service fee. The self-check above can be applied to any provider — including Finboo.

Sources

European Union:

- Directive (EU) 2015/2366 (PSD2) — Article 45(1) on transparency requirements for single transactions; Articles 38(1) and 61(1) on the corporate opt-out. https://eur-lex.europa.eu/eli/dir/2015/2366/oj

- Regulation (EU) 2019/518 amending Regulation (EC) 924/2009 (CBPR2) — FX-transparency requirements. Consolidated text — Regulation (EU) 2021/1230. https://eur-lex.europa.eu/eli/reg/2019/518/oj; https://eur-lex.europa.eu/eli/reg/2021/1230/oj

- European Banking Authority Single Rulebook Q&A 2023_6777 — application of Article 45(1) PSD2 to FX mark-ups. https://www.eba.europa.eu/single-rule-book-qa/qna/view/publicId/2023_6777

- PSD3 and Payment Services Regulation (PSR) — political agreement between the European Parliament and the Council of the EU, November 2025; final text expected in the first half of 2026.

United States:

- 12 CFR Part 1005, Subpart B (Regulation E, Remittance Transfer Rule) — definition of "sender" and the B2B exclusion. https://www.consumerfinance.gov/rules-policy/final-rules/electronic-fund-transfers-regulation-e/

- CFPB Small Entity Compliance Guide for Remittance Transfers, June 2020.

United Kingdom:

- Payment Services Regulations 2017 — UK transposition of PSD2. https://www.legislation.gov.uk/uksi/2017/752/contents

- FCA cross-border payments and FX transparency guidance.